A {Good News} Cancer Update and a {Bad News} Life Update

2024 looked at 2023 and said, “Hold my beer.”

Hey there! If you’re new here, this is a cancer update for my husband, Bryan — not my usual Wednesday newsletter. For the backstory, you can see previous updates HERE. If you’re here for the non-cancer content, I’ll be back on Wednesday with The Usual.

First, the good news.

To recap our last update from November 2023, Bryan’s treatment is in surveillance mode for the next 2-5 years following his “no cancer detected” CT scan in October at the end of his chemotherapy regiment. This involves:

blood tests every three months

annual CT scans

annual colonoscopy

I’m happy to report that his first follow-up blood test, which was taken in January, came back negative for cancer markers! Yay! His next check-in is a colonoscopy scheduled for April – we’ll update again after that.

Now, the bad news.

Just when we thought 2024 would bring a much needed reset for us after our year of colon cancer treatment, Bryan was laid off in early January after four years in his current role, along with 5 others from his team plus another ten from other teams this past week.

On the one hand, we were like, “At least it’s not cancer!” but on the other hand we were like… seriously?!

It’s a bit of a bloodbath in the tech industry right now with thousands of employees getting laid off from local companies like Microsoft, Amazon, and REI in the last year. Bryan has a strong network and a great reputation around town, but this is a job market unlike any we’ve seen in the last 20+ years because there are so many people competing for jobs in his field right now.

He’s finding that companies are pulling job postings after 24 hours because they’re receiving thousands of applications, and he’s had conversations with colleagues who have been out of work for six, seven months, and even a year.

American healthcare is a joke

Complicating this, of course, is our uniquely American healthcare system that is tied to employment. This has made the last few weeks extremely stressful as we navigate our healthcare options for Bryan’s continued cancer surveillance and treatment (because remember, he’s not necessarily cancer free yet). We were spoiled by Bryan’s employer-provided health insurance, which was manageable in every way – monthly premiums and per-visit out of pocket expenses.

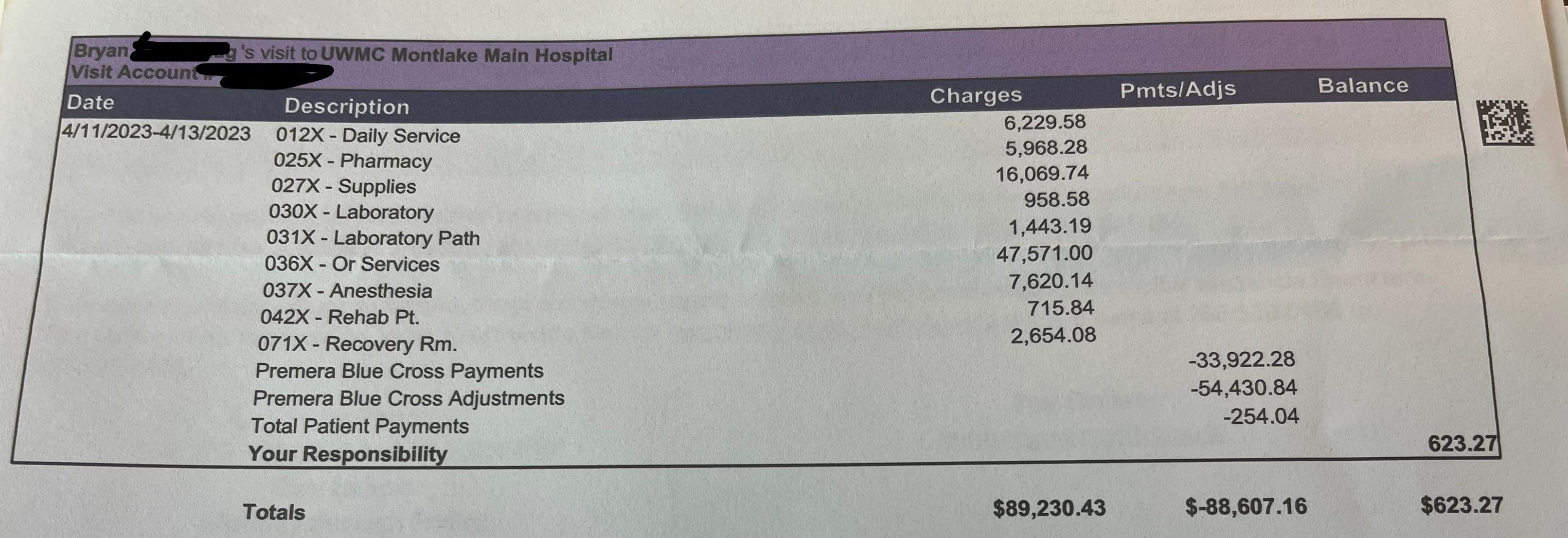

Consider his surgery to have 10” of his colon removed, for example:

Out of $89,000 we paid a little over $600, thanks to a low deductible and a low out-of-pocket maximum. Having met these maximums in April, we paid zero dollars in healthcare costs for the rest of the year, which was incredible considering each of his twelve chemotherapy appointments were approximately $6,000 - $8,000 per visit.

We had to seriously consider the ramifications of moving Bryan to my employer’s health insurance plan, which is a completely different company with its own network of providers. Under my plan, an out-of-network procedure is only covered at 50% and there is no out-of-pocket maximum for out-of-network providers. This means if his oncology providers aren’t part of my plan’s network, a resurgence of his cancer could result in $40,000 to $100,000 (or more) in medical debt.1

In the end, we decided to keep Bryan on his same plan through COBRA benefits2 to ensure a continuity of care for him. The kids and I moved to my employer’s healthcare plan since we are not tied to specific providers. However, the monthly premiums coming out of my paycheck for just the three of us exceed $1,400/month, so this is a huge, new expense for us.

Why am I talking about American healthcare?

The reason I’m bringing up the dysfunction of our American healthcare system is partly to illustrate the struggle of millions of people in this country who are living on the edge of financial ruin with no safety net.

According to The Motley Fool and other sources, 63% of American employees are unable to cover a surprise $500 expense, 76% of employees don’t have enough savings to cover one month of expenses, and over one third of employees earning $100,000 or more are living paycheck to paycheck.

You might argue that this represents a lack of financial planning or discipline, but there is evidence to support how the dramatic rise in housing costs has exponentially outpaced the increase in wages. In Seattle, a $100,000/year salary is not enough to buy a house and is barely enough to cover rent and expenses while living in the city.

I can’t recall if I’ve mentioned this before in my newsletter, but my day job is in communications and fundraising within the nonprofit sector, specifically in the area homelessness and poverty. A few years ago I met a woman through the transitional housing program I was working for at the time who had retired from her career in accounting and got herself a “fun job” in retail – I’ll call her Nancy.

Nancy ended up getting sick, which turned into pneumonia, which landed her in the hospital for a few days. She eventually recovered, but between the hospital bills and lost wages from missing so much work at her hourly job, Nancy couldn’t pay her rent. Why couldn’t she pay her rent, you ask? Look again at that bill I posted for a three-day hospital stay. Without surgery, her bill was likely not that expensive, but if she was uninsured or underinsured, she would have owed far more than $600.

She did all the right things, including reaching out to her landlord proactively to come up with a payment plan, and they were unwilling to work with her. Here’s the kicker: Nancy had been a faithful tenant in her building for ten years. Ten fucking years. And they still evicted her.

Nancy got back on her feet with support from program services, but she spent several months living in shelters while sorting it all out.

I share this story because I’m passionate about humanizing the realities of poverty and homelessness - especially in the city of Seattle where homelessness is dehumanized and there is so much hate and contempt expressed publicly toward the visible signs of homelessness. We are a weird city that claims to be progressive but would rather tuck away our unhoused neighbors where they can’t be seen, and not fund core programs that could make a difference.

Bryan and I are privileged, and I think we’ll be okay. We have some savings and a long runway to work with. But still, I’m nervous because I’ve seen how normal it is to go from having it all to having nothing, and I’m pissed that so much of our stability depends on the whims of billionaire corporations.

I refuse to feel ashamed about our situation because shame drives us to hide and I think in times of stress and vulnerability we need community the most.

Thanks for reading.

If you liked this one, you might also like…

This newsletter from July 2023 explaining the cancer detection blood test and the super cool robot valet parking.

Or this newsletter from May 2023 about Bryan getting his Matrix Port installed and then getting thrown out of a concert venue.

The level of complication to figure this out was insane, because I couldn’t just look up Fred Hutch as a provider to see if the whole care center was in-network. The insurance company contracts with each department, so I would have had to consider all the possible medical scenarios and figure out which department they fall into. No thanks.

COBRA, or the Consolidated Omnibus Budget Reconciliation Act, is a federal law that allows workers and their families who have lost their employer-provided health insurance due to specific life events to continue the same group health coverage for a limited period. Under COBRA, qualified individuals have the opportunity to continue their health benefits temporarily, even when their coverage under the group health plan would otherwise come to an end.

First and foremost, hurray for negative scans!

The healthcare system in this country is beyond broken, and I’m surprised it’s not talked about more. Tbh, I’m surprised we haven’t all taken to the streets to force a change… hard to do when most people are scrambling to make enough to get by, I suppose.

few things are more quintessentially American than having to split insurance coverage between family members. It’s a calculus we run every fall. I’d love it if we never did it again.

I should just say ditto to what Kevin said. No topic gets me more riled up than the U.S. healthcare industry. No one, not doctors, administrators, insurance agents, not even most multi-millionaires, like our system of cruelty, ineptitude, bribery, corruption, inhumanity…I could go on and on.

And I’m learning more and more about the systemic elder abuse inherent in Medicare as I take care of my 81 year old aunt. Oy.

No wonder we have an epidemic of anxiety.

Oh, happy Sunday! Go Niners!😜